The Maine market outperformed New England in sales while also showing a rise in prices, aligning with earlier predictions.

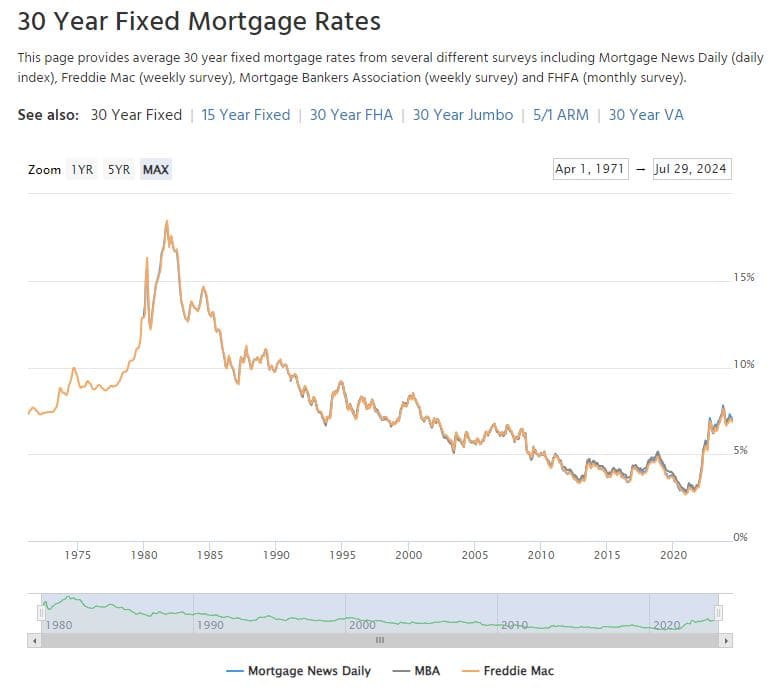

Last year, many sellers hesitated to list their properties due to the low interest rates secured during the Covid era, making it difficult to accept current rates of around 7%. These rates are unlikely to change dramatically soon, and over the past six months, sellers have begun to move past them and list their properties.

Sellers typically list their homes only when necessary or due to significant life changes. Events such as divorces, expanding families, relocations, and downsizing have driven the market, but these factors haven’t significantly boosted inventory to meet demand. As a result, average housing prices have continued to rise.

Buyers are determined to find homes within their budgets, now lower due to rising rates and prices. Monitoring rates and keeping pre-approvals up-to-date is crucial to be ready to strike if rates drop.

Homeownership offers advantages over renting, including full control over your living space, fixed monthly payments, and asset growth through equity. Mortgage interest is often tax-deductible, especially in the early loan stages.

At mid-year, sellers face varied market conditions. The first half of the year tends to favor sellers, while the second half leans towards buyers. Listing your property now can still be beneficial. Setting a competitive price can attract more buyers and give you greater control over negotiations. Sellers should not wait, as hoping for lower rates might mean missing out on the perfect home. If rates drop and prices remain steady, refinancing can help secure a lower interest rate.

National factors affecting the market include commission changes and the election. The commission class action settlement will alter how real estate commissions are handled, causing some confusion. Starting in August, sellers may only need to pay their agent’s commission, while buyers will cover their agent’s fees out of pocket. This change would have impacted VA buyers, but a temporary amendment allows their benefits to continue. Buyer affordability might be affected since this fee can’t be included in the mortgage. The election year may slow down the real estate market this winter, but a faster-paced market is expected in 2025 once the changes settle.

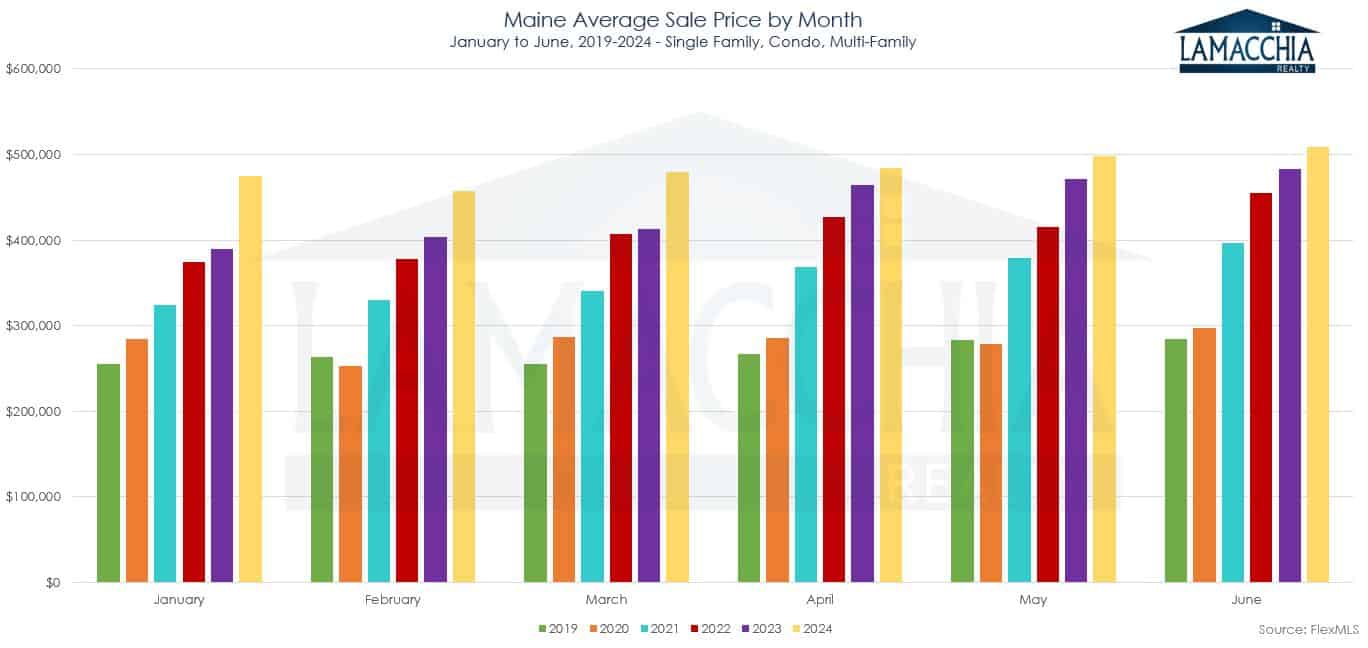

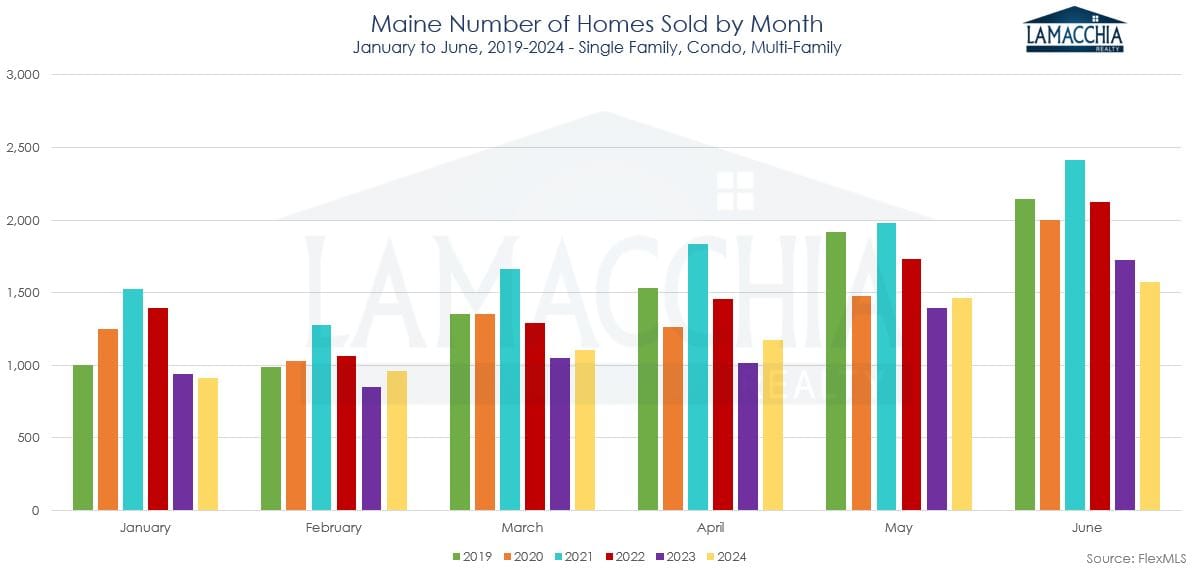

Data provided by FlexMLS then compared to the prior year.

spike due to frenzied demand and since then a drop just hasn’t happened due to low inventory (see yellow line in chart to right). The high demand will make it very unlikely that we will see a price drop.

spike due to frenzied demand and since then a drop just hasn’t happened due to low inventory (see yellow line in chart to right). The high demand will make it very unlikely that we will see a price drop.